Card-based payments now dominate veterinary checkout. Clients increasingly use rewards cards, financing options, and digital payment methods to manage the cost of care — tools that are useful for them but carry acceptance costs for the practice.

Unlike fixed costs such as rent or utilities, card processing fees move with transaction volume, card type, and pricing structure. That variability makes them easy to absorb without scrutiny. If you aren't reviewing your merchant statements regularly, you may be paying processor markups or unfavorable pass-through rates that are worth examining and, in some cases, renegotiating.²

For practices at $1M in revenue or above, processing fees are no longer a minor line item. The math is worth running.

Veterinary practices typically pay between 2.5% and 3.5% per transaction, with some paying closer to 3%–4% depending on their processor and card mix.³ Using the low end of that range: a practice with $900K in annual card volume pays around $22,500 a year at a 2.5% effective rate, or $112,500 over five years. At $1.8M in card volume that climbs to $45,000 a year; at $3.6M it reaches $90,000. Because these costs recur every year, even modest reductions in your effective rate free up dollars for other priorities.

In an environment of rising wages and persistent staff shortages, that figure represents real optionality. The same dollars currently going to a processor could fund annual bonuses or benefits improvements that support retention. They could go toward diagnostic equipment, dental imaging, or other capital investments that expand what your practice can offer. They could fund outreach to lapsed clients — a population that, for many practices, represents a significant share of recoverable revenue.⁴

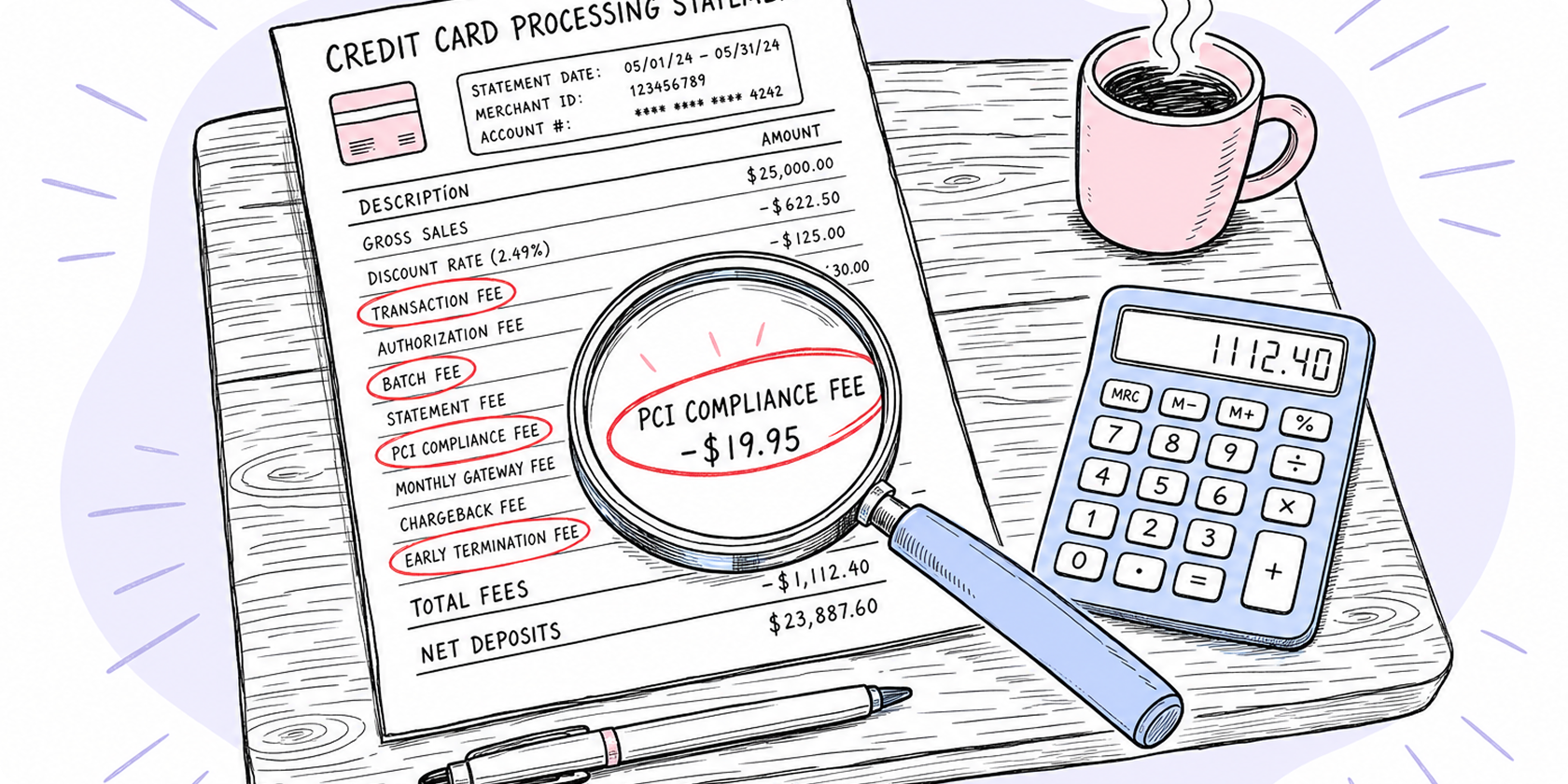

Most owners overlook processing fees in budgeting because the cost is spread across hundreds of individual transactions and only surfaces when you pull merchant statements and do the math.

.png)

For some practices, a properly structured surcharging program can offset a meaningful portion of credit card acceptance costs. Client response depends significantly on how clearly the practice communicates the fee and whether a no-fee payment option exists alongside it.

Research on pricing transparency more broadly finds that consumers respond well to disclosed fees when they have a genuine alternative — the fee reads as a choice rather than a hidden cost. Practices that apply that principle consistently — clear signage, a no-fee option at checkout, and staff who can explain the structure plainly — tend to see less friction than those that add a surcharge without context.

Regular audits of your merchant services can also surface hidden markups that, once removed, improve your effective rate independent of any surcharging program.

**Surcharge rules vary by state and card network. Surcharges may be prohibited, capped, or subject to specific disclosure and receipt requirements in some jurisdictions. As of 2026, surcharging is prohibited in Connecticut, Massachusetts, and Maine, and subject to additional caps or restrictions in some other states. Debit and prepaid cards may not be surcharged under any circumstances, even if processed as credit. Before implementing a surcharge program, confirm the rules that apply to your practice, processor, card networks, and location.**⁵

¹ Illustrative calculation based on a 2.5% effective processing rate applied to card payment volume. Assumes a majority of practice revenue is collected via card. Actual fees depend on effective rate, card mix, and transaction volume. Industry benchmarks put the typical veterinary processing rate at 2.5%–3.5%, with some practices paying 3%–4%. Sources for rate range: AAHA Trends, "Improving Cash Flow and Eliminating Credit Card Fees in Veterinary Practices," May 2026: https://www.aaha.org/trends-magazine/publications/improving-cash-flow-and-eliminating-credit-card-fees-in-veterinary-practices/ — Vellis Financial: https://www.vellis.financial/blog/vellis-news/veterinary-credit-card-processing-fees

² Vellis Financial, ibid. — Vida AI, "Veterinary Credit Card Processing: Complete Guide for Practices": https://vida.io/blog/veterinary-credit-card-processing

³ AAHA Trends, ibid. ("Most practices are paying between 3% and 4% on every transaction") — Vellis Financial, ibid. ("On average, veterinary credit card processing fees range between 2.5% and 3.5% per transaction")

⁴ Staff turnover context: AVMA, "Benchmarking Data Plus Elevating Efficiency Equals Practice Productivity," October 2025: https://www.avma.org/news/benchmarking-data-plus-elevating-efficiency-equals-practice-productivity — Client recapture context: iVET360 2025 Veterinary Industry Benchmark Report (new client acquisition down 9.5% in 2024), via Today's Veterinary Business: https://todaysveterinarybusiness.com/ivet360-report-042625/

⁵ Surcharging state restrictions: Scratchpay surcharging page (CT, MA, ME): https://scratchpay.com/surcharging/ — Veterinary Practice News, "Should You Implement Credit Card Surcharges?," November 2025: https://www.veterinarypracticenews.com/implementing-credit-card-surcharges/ — Nadapayments, "Vet Clinic Credit Card Processing Fees": https://www.nadapayments.com/blog/vet-clinic-credit-card-processing-fees

We believe patients deserve access to affordable care.

As the leader in payment processing and financing for veterinary practices across the U.S. and Canada, we’re creating products and services that simplify and add delight to patient and practice experiences.

FOLLOW US

GET THE APP

Scratch Pay plans in the U.S. are issued by WebBank. Scratch Pay plans in the U.S. are subject to eligibility and may not be available in all states.

In Canada, loans are issued by Scratch Financial, Inc.

Scratch Financial, Inc. DBA Scratchpay (NMLS ID 1582666).

© 2026 Scratch Financial, Inc. All Rights Reserved.

Scratch, Scratch Pay, Scratchpay, Scratch Checkout, and the Heart Logo are trademarks of Scratch Financial, Inc.